Asian Markets and Geopolitical Tensions: Recovery and Risks

Market Background: Immediate Relief After Diplomatic Pause

Asian markets steadied on March 24, 2026, after President Trump delayed threatened strikes on Iran, signaling a possible diplomatic path and easing immediate fears of a sudden shock to global oil supply and regional risk assets. While this pause did not resolve the underlying conflict, it provided a temporary reprieve, reducing near-term pressure long enough for equities and credit in Asia to recover modestly. This regional rebound followed a cautious relief handover from Wall Street, demonstrating that investors were taking their cues from overnight U.S. sentiment rather than embracing a full risk-on turn.

Asian Market Recovery and Sectoral Responses

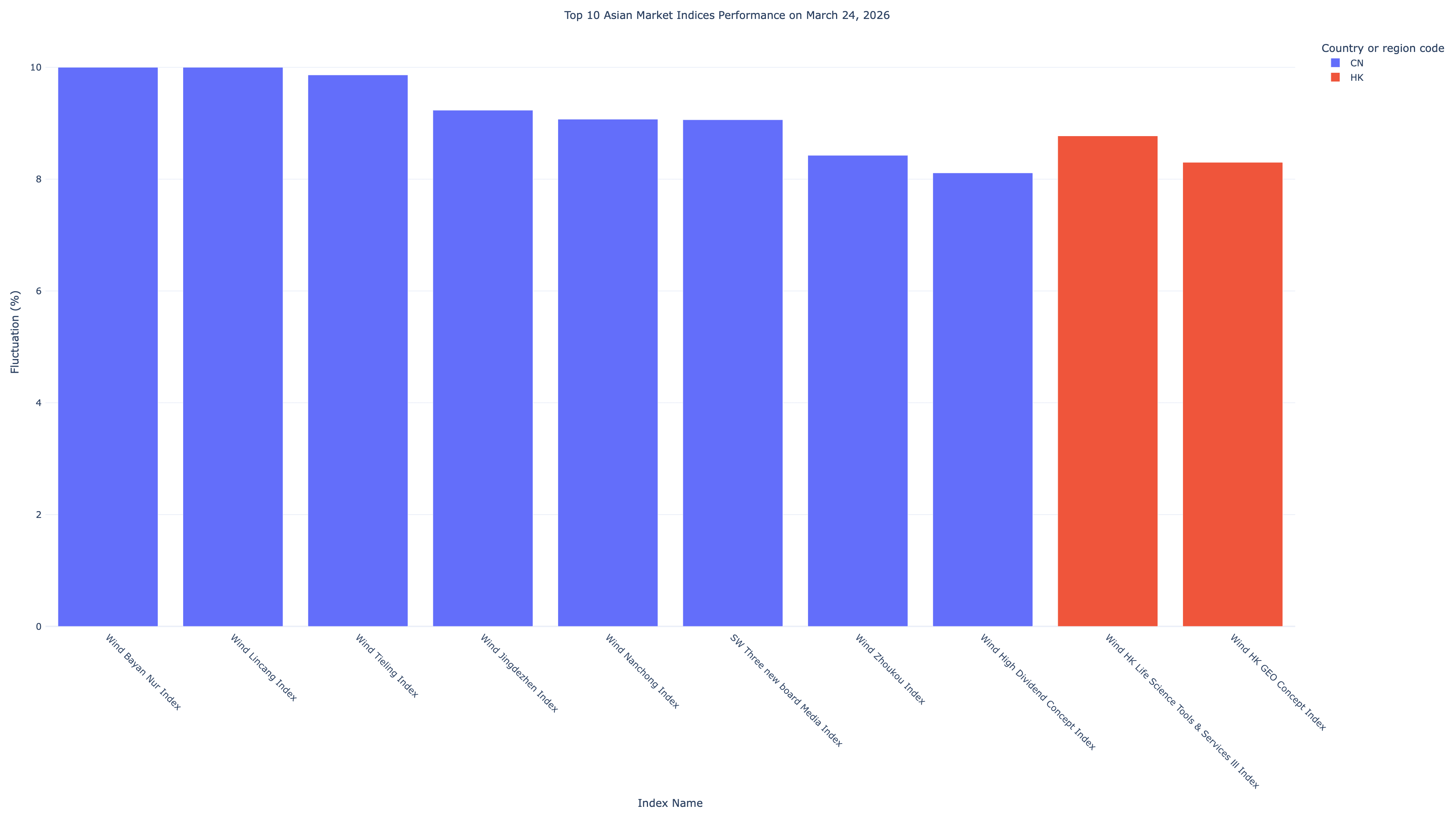

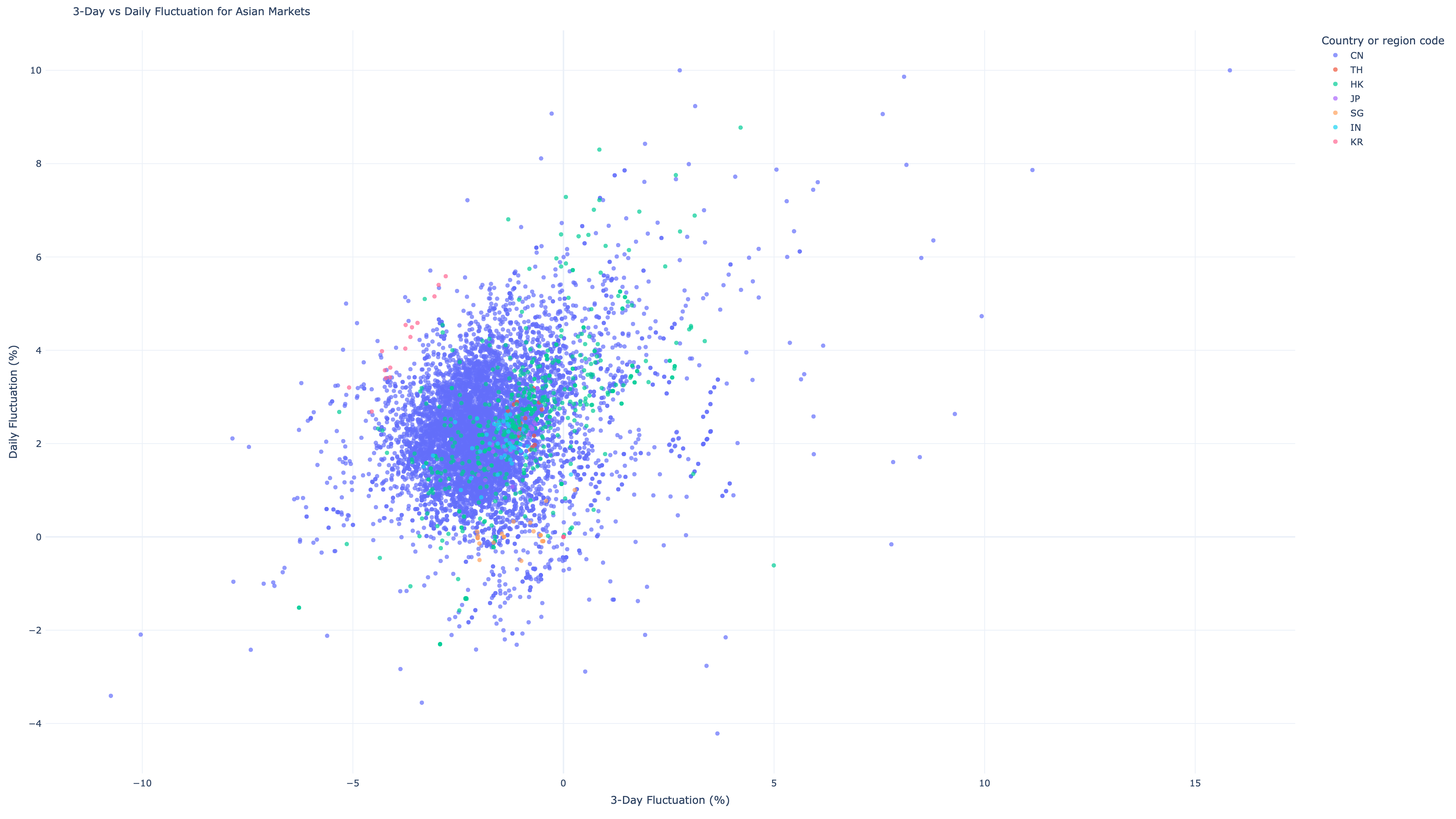

The delayed military action triggered a broad-based recovery across Asian markets on March 24, with most markets showing positive performance and gains ranging from 1.8% to 10.0%. This classic "buy the dip" pattern was particularly evident in markets that had experienced significant declines in the preceding days.

- Regional Leadership: Chinese markets led the rebound, with the CJSC Raw Materials Index (+2.80%) and CJSC Industry Index (+2.02%) showing strong recovery. In Japan, stocks rose in early trading, with insurers among the notable gainers as financial names reacted quickly to the lower perceived odds of an imminent strike on energy infrastructure. Meanwhile, India's Sensex rallied 2% (1,500 points) on hopes of de-escalation, highlighting the sensitivity of emerging markets to geopolitical risks, especially after significant foreign capital outflows earlier in the month.

- Sectoral Vulnerabilities: High-growth tech and AI stocks—including Amazon, Nvidia, and TSMC—were caught in the crossfire earlier in March, exacerbated by attacks on AWS data centers.

- Credit Market Recovery: Funding-market signals turned positive as Asian corporate bond markets rebounded alongside equities, indicating that the relief reached regional financing conditions rather than stopping solely at stock indexes.

Oil Price Volatility and Unresolved Supply Risks

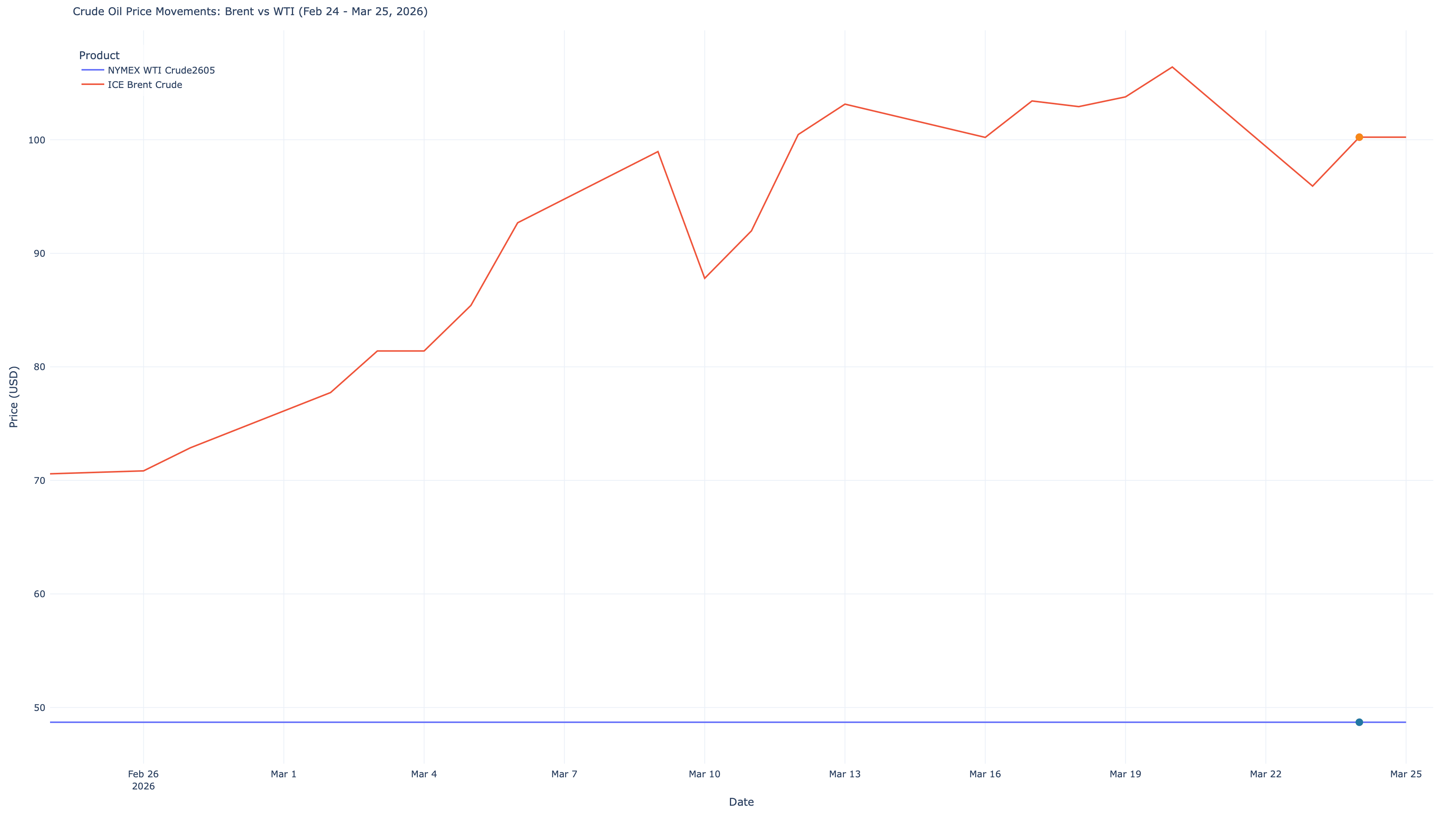

The geopolitical tension led to intense volatility in the energy markets. Brent crude spiked to 100.23 by March 24. Notably, the spread between WTI and Brent narrowed during the crisis period, underscoring global market integration in risk pricing.

However, the relief was short-lived. Oil prices resumed their climb shortly after the initial drop, highlighting how quickly traders refocused on unresolved supply risks. With Asian economies remaining highly vulnerable to any future escalation affecting shipping in the Strait of Hormuz—which facilitates 20% of global oil trade—the threat to Iranian energy infrastructure remains a critical concern.

Investment Strategy Implications

The diplomatic pause provided breathing room for risk assets, but the underlying tensions necessitate careful strategic positioning:

- Temporary Reprieve vs. Long-Term Risk: The situation offers short-term relief, but long-term risks remain prominent. Defensive rotation has been evident, with energy and defensive sectors outperforming during the height of the crisis.

- Currency and Regional Differentiation: USD/Asian currency pairs showed limited movement, suggesting markets viewed the immediate event as contained. Furthermore, Northeast Asian markets (Japan, Korea) exhibited different risk profiles compared to Southeast Asian markets, reflecting varying degrees of energy dependence and trade exposure.

Actionable Watchpoints and Risk Scenarios

Investors should monitor key indicators to navigate the ongoing uncertainty:

- What to Monitor: Keep a close eye on concrete diplomatic progress or further de-escalation measures, weekly EIA oil inventory data, changes in shipping insurance premiums for vessels transiting the Persian Gulf, and mentions of Middle East exposure in upcoming Q1 2026 corporate earnings calls.

- Risk Scenarios:

- Base Case (60%): Continued diplomatic engagement with occasional flare-ups. Oil prices stabilize around the 105 range.

- Bear Case (25%): Renewed escalation leading to actual military action, pushing Brent crude spikes above $120.

- Bull Case (15%): A comprehensive agreement is reached, effectively removing the geopolitical premium from oil prices.