Estée Lauder and Puig Potential Combination: Strategic Rationale and Market Reaction

Current Market Position: A $40 Billion Beauty Giant in the Making?

As of March 25, 2026, Estée Lauder (EL.N) and Spanish beauty group Puig find themselves in preliminary discussions regarding a potential combination. Financial Times reports suggest this deal could create a combined beauty powerhouse valued at approximately $40 billion.

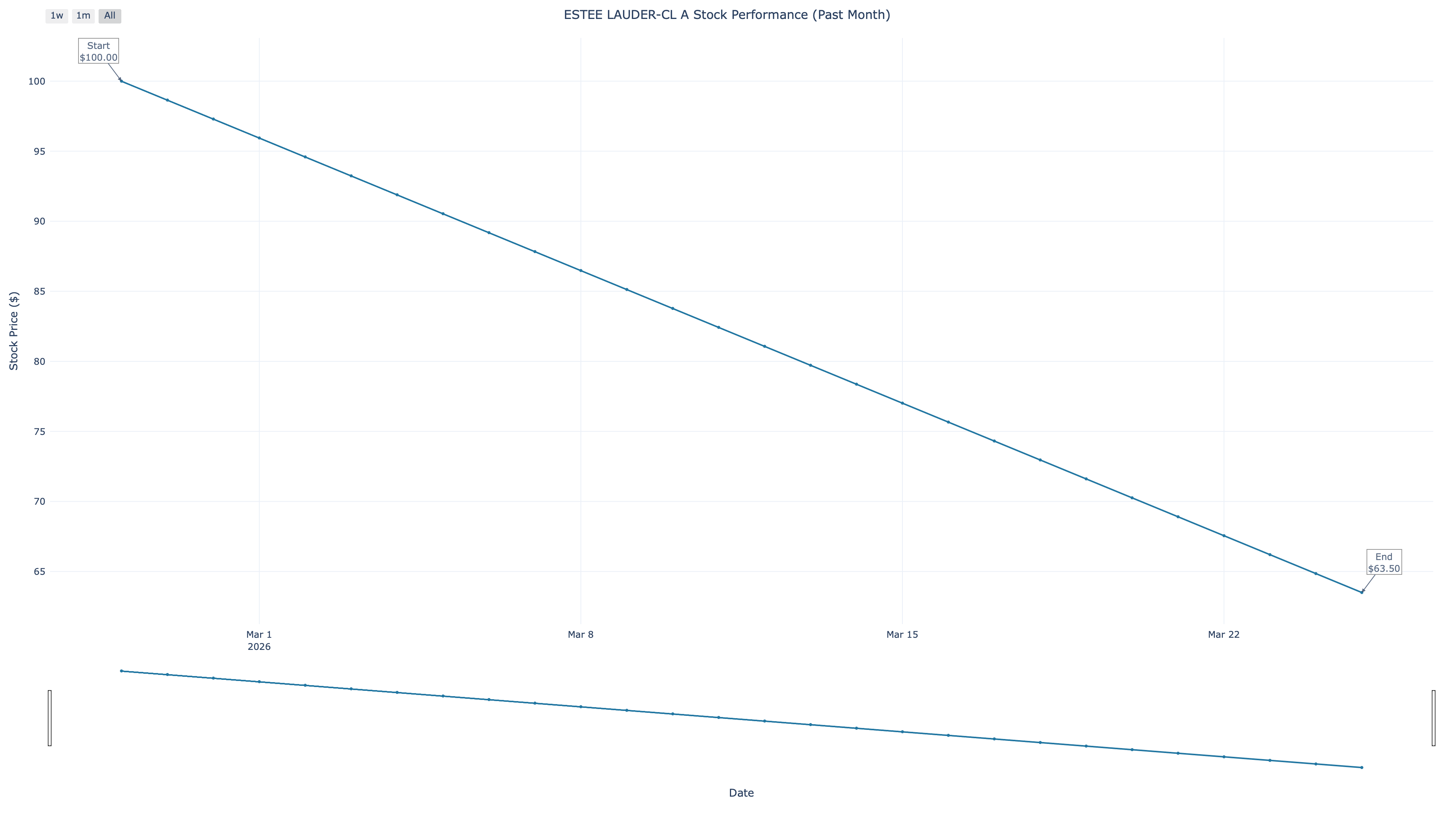

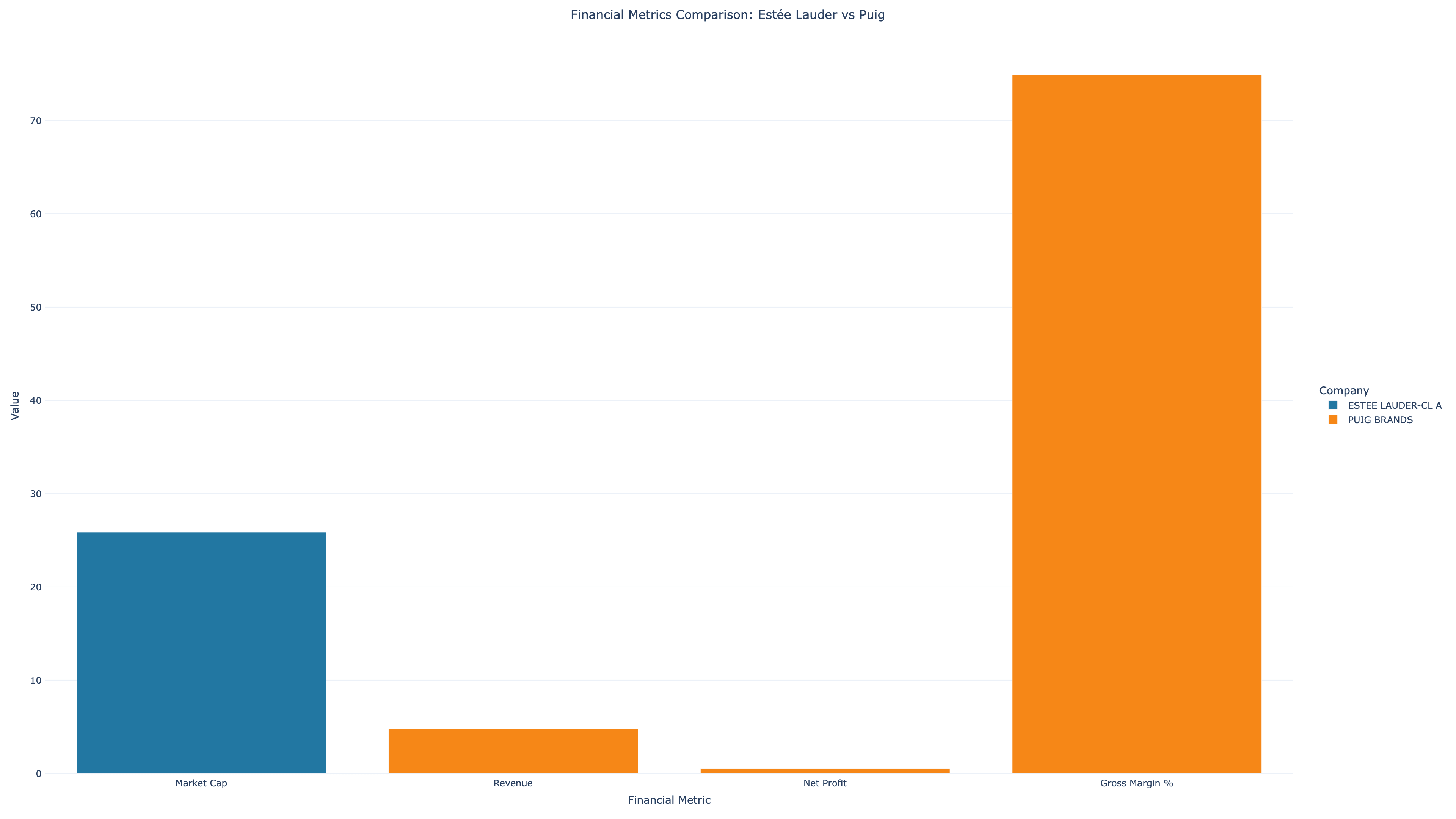

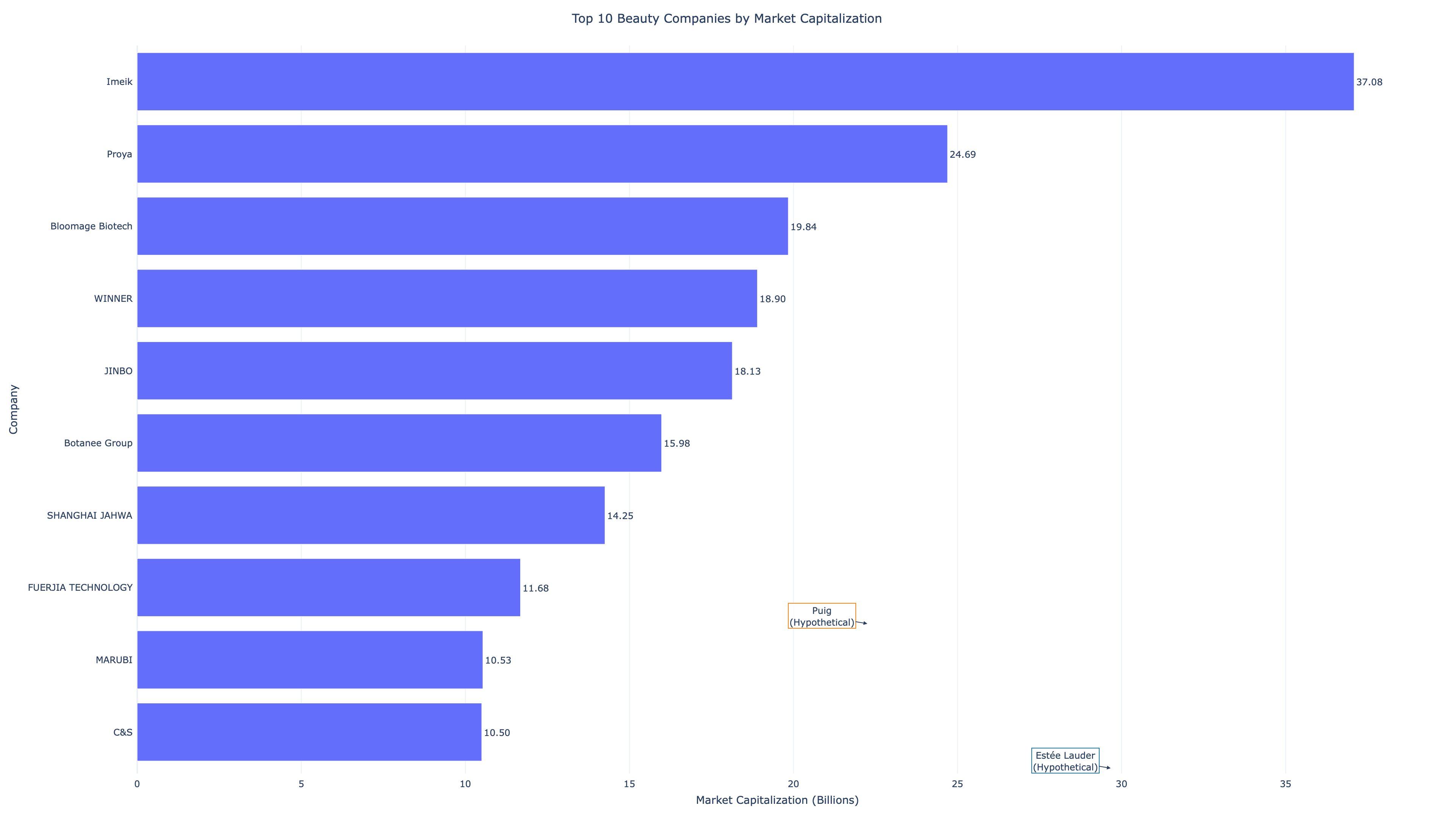

Estée Lauder enters these talks from a position of recent weakness, grappling with sluggish demand in the U.S. market. The company’s stock has declined 36.5% over the past month, with its market capitalization standing at $25.86 billion.

In contrast, Puig brings strong financial metrics to the table, boasting €4.79 billion in revenue, a robust 74.91% gross margin, and an estimated market cap of $10.2 billion. While the structure—whether a merger, combination, or acquisition—remains fluid, the potential deal is likely to involve a mix of cash and stock.

Market Reaction Divergence and Structural Implications

The news triggered a striking divergence in market sentiment:

- Asymmetric Market Response: While Puig's stock surged 13-15% upon the news, Estée Lauder's shares declined by 7.72% on the announcement day. This asymmetry suggests Puig shareholders see immediate upside in joining a larger entity, whereas Estée Lauder investors remain deeply skeptical.

- Scale and Negotiation Power: Despite current challenges, Estée Lauder’s market cap is roughly 2.5 times larger than Puig's, indicating this would operate more as a strategic acquisition. A combined $40 billion entity would position the new company as a formidable challenger to industry giants like L'Oréal and Procter & Gamble, providing massive economies of scale and enhanced negotiating power with global retailers.

Strategic Rationale: The Turnaround and Fragrance Focus

Estée Lauder is undeniably in the midst of a broader corporate turnaround. This proposed combination is deeply anchored in multiple strategic imperatives:

- Accelerating the Turnaround: A combination with Puig provides Estée Lauder with immediate access to a highly profitable prestige portfolio and bolsters its presence in the European market.

- Doubling Down on Fragrance: As noted by Reuters, expanding the fragrance category is a central element of this potential deal. Following its $2.8 billion acquisition of Tom Ford in 2022, acquiring Puig’s iconic assets—including Rabanne, Carolina Herrera, and Jean Paul Gaultier—would cement Estée Lauder's dominance in luxury prestige fragrance, creating a comprehensive beauty portfolio.

- Preserving Cash: Utilizing stock as part of the deal structure helps Estée Lauder preserve crucial cash reserves needed for its ongoing internal turnaround initiatives, while keeping Puig shareholders invested in the long-term success of the combined entity.

Actionable Insights and Critical Risks

For investors and industry observers, the weak share response for Estée Lauder underscores that a deal alone does not inherently fix structural business problems. Important factors to monitor include:

- Integration Execution is Paramount: The ultimate success of this combination will hinge on the seamless integration of supply chains, overlapping portfolios, and vastly different corporate cultures (Puig’s Spanish family-controlled heritage versus Estée Lauder’s U.S. public structure). Missteps could severely exacerbate Estée Lauder's existing operational issues.

- Regulatory Scrutiny: A $40 billion beauty merger will inevitably attract intense antitrust scrutiny in both the US and the EU, particularly concerning overlapping luxury fragrance and skincare categories.

- Brand Portfolio Rationalization: With a colossal umbrella of brands ranging from Clinique and Bobbi Brown to Tom Ford and Rabanne, clear brand architecture and strategic focus will be essential to avoid market cannibalization.

- Turnaround Distraction: The most critical immediate risk is that complex, high-stakes M&A negotiations could fatally distract Estée Lauder’s management from executing its core turnaround plan. If same-store sales continue to erode while leadership is focused on the deal, investor confidence may plunge further.