Global Carmakers' EV Strategy Shift: A Costly Retreat or Prudent Adjustment?

Market Facts & Data: The Rapid Evolution of Transportation

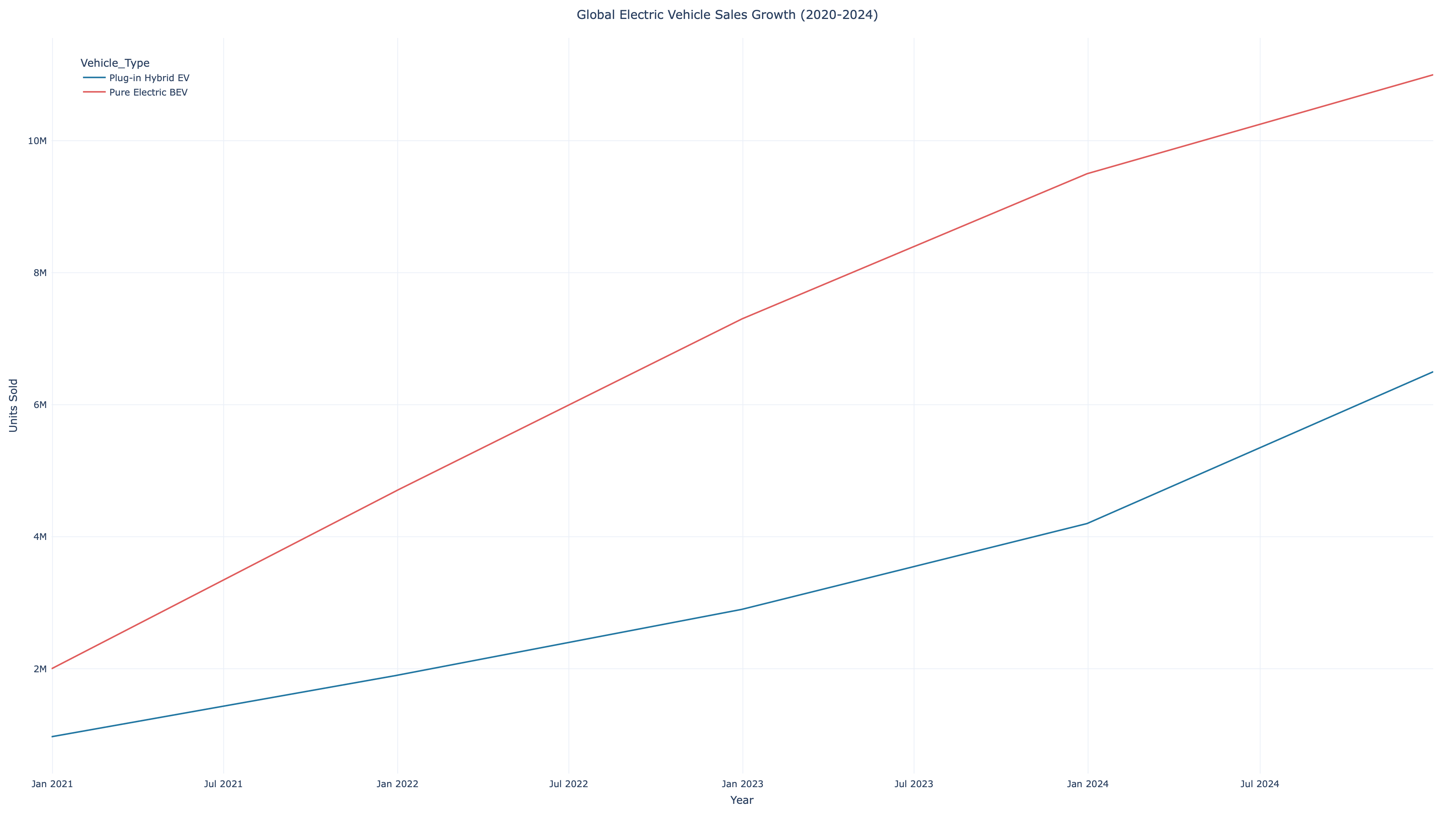

Between 2020 and 2024, the global automotive landscape completely transformed. Battery Electric Vehicles (BEVs) saw an astonishing 450% growth, surging from 2 million to 11 million units sold. Concurrently, Plug-in Hybrid Electric Vehicles (PHEVs) expanded by 570%, jumping from 970,000 to 6.5 million units.

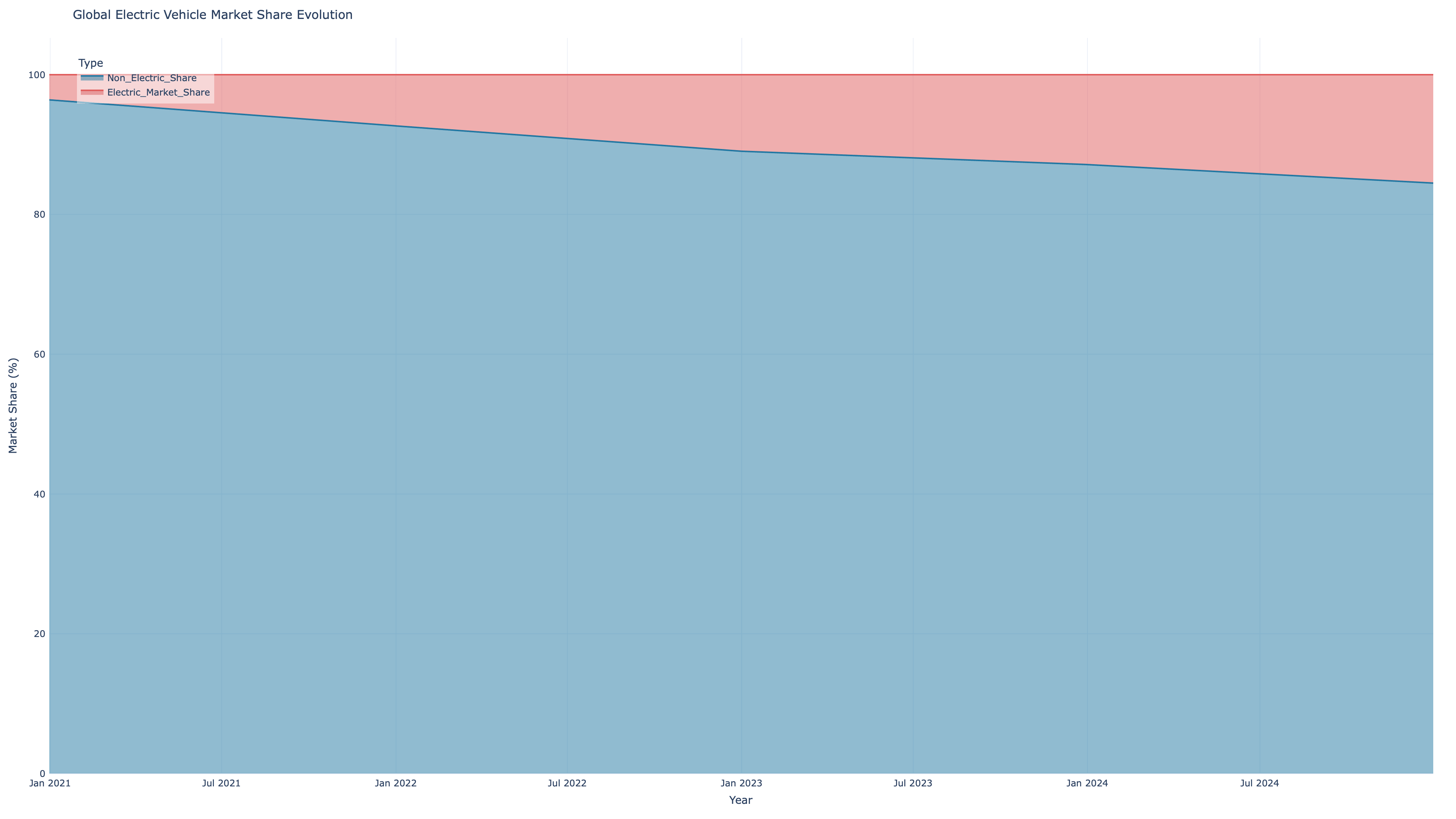

Consequently, the total global EV market share expanded aggressively from 3.7% in 2020 to 18.4% by 2024, squeezing the traditional internal combustion engine (ICE) footprint from 96.3% down to 81.6%.

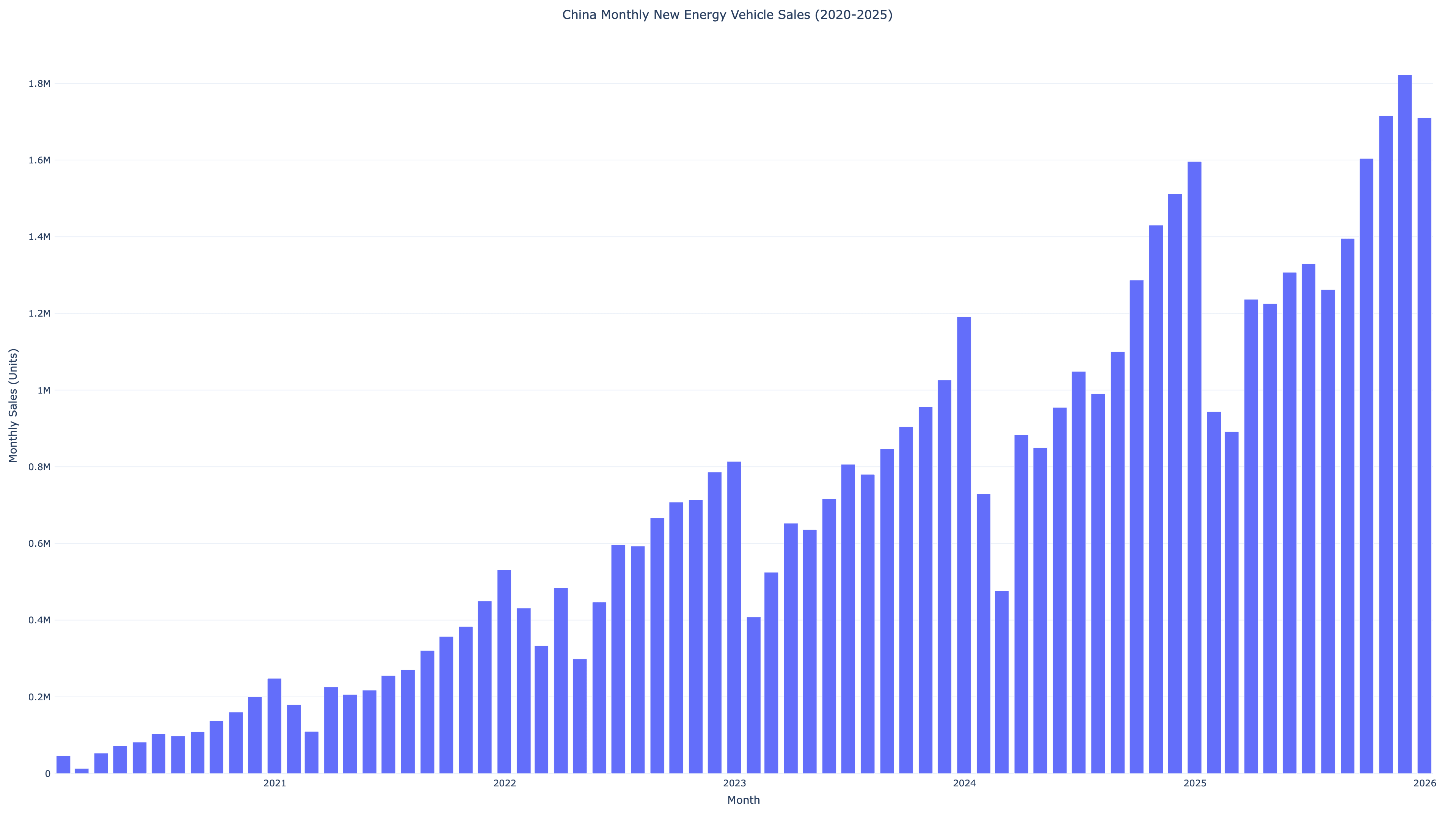

A dominant driver of this global shift has been China’s explosive New Energy Vehicle (NEV) market. Monthly sales in China grew 36-fold from approximately 46,000 units in early 2020 to 1.71 million units by late 2025. This massive scale has endowed Chinese EV manufacturers with unrivaled advantages in proprietary technology, global supply chains, and absolute cost control, culminating in a collective market capitalization of $2.26 trillion—roughly 84% of the global EV manufacturer market cap.

The Western Retreat: Balancing Demands

Despite these long-term trends, a stark divergence is emerging in corporate strategies. According to recent Financial Times coverage, more than a dozen major global automotive groups, recently joined by Rolls-Royce, are actively scaling back their earlier EV expansion timelines. This pivot is a reaction to a near-term reality: consumer demand for traditional ICE models has remained surprisingly robust, delivering consistent short-term margins.

Western carmakers find themselves trapped in a classic innovator’s dilemma. Managing the heavy, long-term capital investments required to transition a massive manufacturing base while maintaining current quarterly profitability is proving extraordinarily difficult, especially when traditional ICE vehicles still deliver reliable gross margins between 15% to 25%.

However, as reported by The Guardian, leading industry experts and former auto executives warn that refocusing on ICE cars is a "profound strategic mistake." Pulling back now could permanently weaken Western groups just as oil prices climb and global consumer preferences continue to structurally shift toward electric transport.

Investment Insights to Monitor

This divergence separating Western hesitance from aggressive Chinese expansion offers critical signals for investors:

- Profitability Discrepancies: The core driver of the Western pullback is the profitability gap. While legacy automakers lean on reliable ICE margins (15-25%), pure-play EV manufacturers still face steep profitability hurdles. Investors must scrutinize if and how these legacy companies use ICE cash flows to ultimately fund their EV transitions rather than abandoning them.

- The Global Push of Chinese EVs: Armed with extreme scale and cost advantages, Chinese EV makers are no longer confined to their domestic market. Between 2020 and 2024, BEV sales in key European markets like the UK, Germany, and France multiplied 2-3 times over. Chinese manufacturers are actively capitalizing on this structural growth, presenting a direct threat to legacy brands in these regions.

- The Rise of the "Multi-Path" Strategy: Rather than an "all-electric" mandate, legacy automakers may formalize more flexible, multi-technology roadmaps encompassing ICE efficiency improvements, plug-in hybrids, and hydrogen alternatives. Watch for which companies utilize this strategy as a smart bridge versus a permanent crutch.

Systemic Risks in the Current Landscape

- Strategic Misjudgment: If global EV adoption curves accelerate faster than anticipated, legacy manufacturers backing away from EVs now face a permanent loss of market share that cannot readily be won back.

- Regulatory Pressures: Evolving emissions mandates and government incentive programs could forcefully accelerate the phase-out of traditional combustion engines, stranding the assets of companies over-invested in ICE infrastructure.

- Supply Chain Vulnerability: China currently dominates essential battery materials and component supply chains. Western makers slowing their domestic EV investments will face massive security and cost-control hurdles when they eventually restart their EV drives.

- Consumer Preference Shifts: As charging networks expand globally and battery tech continuously improves, consumer anxiety ranges dissolve. A sudden inflection point in mass adoption could leave legacy automakers without competitive stock to supply the market.